Singapore Alcoholic Drinks Market Outlook to 2029

By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region

Report Overview

Report Code

TDR0057

Coverage

Asia

Published

October 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled "Singapore Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region " provides a comprehensive analysis of the alcoholic drinks industry in Singapore. It covers an overview of the industry, market size, market segmentation, key trends, regulatory environment, customer profiles, challenges, and a competitive landscape. The report concludes with future market projections based on revenue, product categories, regions, and success case studies highlighting significant opportunities and potential risks.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled "Singapore Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region " provides a comprehensive analysis of the alcoholic drinks industry in Singapore. It covers an overview of the industry, market size, market segmentation, key trends, regulatory environment, customer profiles, challenges, and a competitive landscape. The report concludes with future market projections based on revenue, product categories, regions, and success case studies highlighting significant opportunities and potential risks.

Singapore Alcoholic Drinks Market Overview and Size

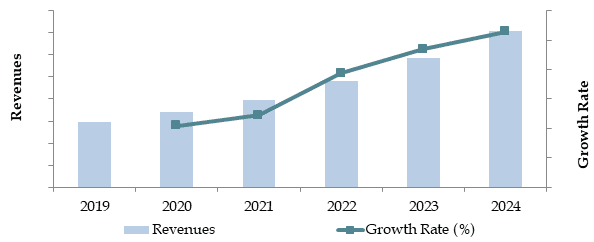

The Singapore alcoholic drinks market reached an estimated value of SGD 1.5 Billion in 2023, driven by evolving consumer preferences, a strong tourism industry, and an increase in premiumization. The market is characterized by key players like Asia Pacific Breweries, Diageo, Pernod Ricard, and Beam Suntory. These companies dominate the market through strong distribution networks, premium product offerings, and tailored marketing strategies aimed at Singapore’s affluent population and expatriate community.

In 2023, the premium alcoholic drinks segment, particularly craft beer and artisanal spirits, experienced significant growth as consumers shifted towards high-quality and unique drinking experiences. Singapore’s vibrant nightlife, strong expatriate presence, and status as a global business hub further bolster demand for premium alcoholic beverages.

Market Size for Singapore Alcoholic Drinks Industry on the Basis of Revenue, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of Singapore Alcoholic Drinks Market

Tourism Boom: Singapore's status as a major tourism hub contributes significantly to the growth of the alcoholic drinks market. In 2023, tourist arrivals increased by 15%, spurring demand for alcoholic beverages, especially in hospitality venues like hotels, bars, and restaurants.

Premiumization Trend: Singaporeans are increasingly gravitating towards premium alcoholic drinks as disposable incomes rise, and consumers seek premium and craft products. This has led to a surge in demand for high-end spirits, fine wines, and artisanal beers.

Health-Conscious Consumers: The rise in health-conscious consumers has fueled demand for low-alcohol and alcohol-free options. In 2023, low-alcohol beer sales grew by 12%, reflecting a shift towards healthier choices while maintaining social drinking habits.

Which Industry Challenges Have Impacted the Growth of Singapore Alcoholic Drinks Market

High Taxes and Duties: Singapore has one of the highest alcohol taxes in the world, which significantly affects the price of alcoholic beverages. The high cost deters many price-sensitive consumers and limits the market for lower-end products. In 2023, excise duties made up over 60% of the retail price of alcoholic beverages, particularly affecting mass-market beer and spirits sales.

Regulatory Restrictions: Strict regulations around alcohol sales, including limited sale hours and restrictions on public consumption, particularly in designated zones, have impacted market growth. For instance, in 2023, the implementation of the Liquor Control Act, which restricts retail sales of alcohol between 10:30 PM and 7:00 AM, led to a decrease in sales during late-night hours, particularly affecting convenience stores and bars.

Health and Social Concerns: Rising health consciousness and government initiatives to reduce excessive drinking have also curbed growth. Campaigns highlighting the negative impacts of alcohol consumption, along with a growing trend towards healthier lifestyles, have led to a slight decline in alcohol consumption per capita. In 2023, alcohol consumption in Singapore decreased by 5%, as more consumers opted for low-alcohol or alcohol-free alternatives.

What are the Regulations and Initiatives which have Governed the Singapore Alcoholic Drinks Market:

Alcohol Licensing and Sales Restrictions: The Singaporean government enforces strict regulations around the sale and distribution of alcoholic beverages. Retailers and hospitality venues must obtain liquor licenses to sell alcohol, and there are strict limits on the hours during which alcohol can be sold. Under the Liquor Control (Supply and Consumption) Act, alcohol sales are prohibited from 10:30 PM to 7:00 AM in retail outlets. This regulation, introduced in 2015, aims to reduce alcohol-related public disturbances, particularly in high-traffic areas.

Excise Duties on Alcohol: Alcoholic beverages in Singapore are subject to one of the highest excise duties globally. In 2023, the excise duty for beer stood at SGD 60 per liter of alcohol content, while for spirits it reached SGD 88 per liter. These duties significantly affect retail prices, making Singapore one of the most expensive markets for alcohol. The high excise rates are intended to curb excessive alcohol consumption and generate revenue for public health initiatives.

Public Consumption Regulations: Public consumption of alcohol is strictly regulated in Singapore. Under the Liquor Control Act, drinking in public spaces is prohibited between 10:30 PM and 7:00 AM, with stricter rules applied in designated Liquor Control Zones. These regulations are enforced to maintain public order and minimize alcohol-related disturbances, especially in areas such as Little Singapore and Geylang.

Singapore Alcoholic Drinks Market Segmentation

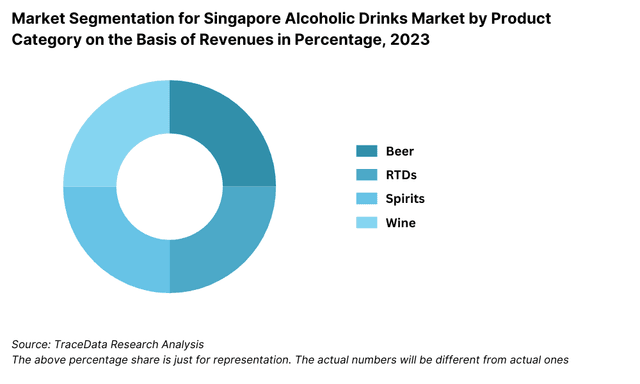

By Product Category: Beer continues to dominate the Singapore alcoholic drinks market, driven by high consumption rates in social settings and its relatively lower cost compared to spirits. The craft beer segment is also growing, fueled by an increasing consumer preference for unique and locally brewed beverages. Spirits hold a significant market share due to the demand for premium and high-quality products, particularly among expatriates and tourists. Wine consumption is on the rise, especially among high-income groups and those seeking a more refined drinking experience.

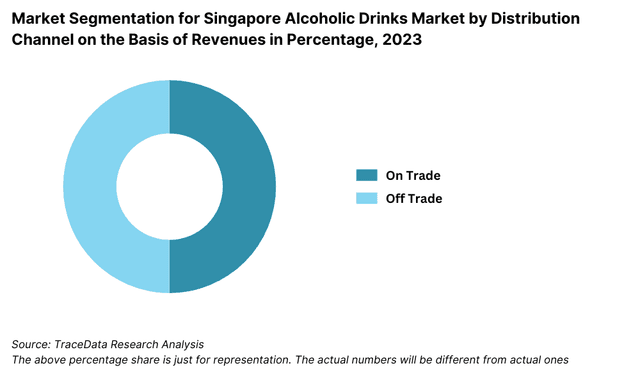

By Distribution Channel: On-trade channels, such as bars, restaurants, and hotels, remain the dominant distribution method, contributing significantly to overall sales due to Singapore’s vibrant nightlife and tourism sector. Off-trade sales, including retail stores and supermarkets, have been growing due to the convenience of purchasing alcohol for home consumption. The rapid rise of e-commerce platforms has also contributed to off-trade sales, as online alcohol delivery services become increasingly popular.

By Consumer Demographics: Younger consumers, particularly those aged 18-35, drive demand for beer and trendy cocktails in Singapore’s social and nightlife scenes. This group is also more likely to explore new product categories, such as craft beers and alcohol-free alternatives. Meanwhile, high-income earners and expatriates tend to prefer premium wines and spirits, contributing significantly to the growth of premium alcoholic beverages.

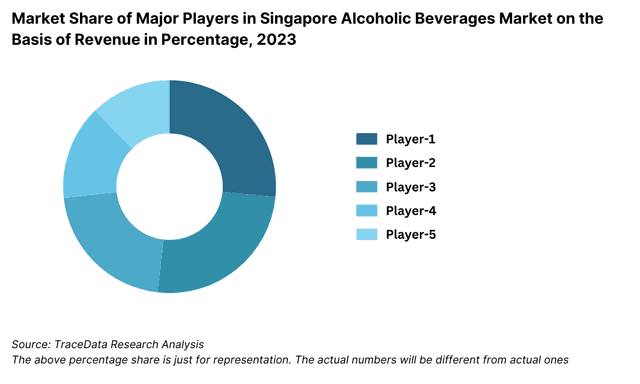

Competitive Landscape in Singapore Alcoholic Drinks Market

The Singapore alcoholic drinks market is highly competitive, with a mix of both local and international players. Major companies such as Asia Pacific Breweries, Diageo, Pernod Ricard, Beam Suntory, and Moët Hennessy dominate the market through their established brands, extensive distribution networks, and aggressive marketing strategies. Meanwhile, the rise of smaller craft breweries and artisanal spirit producers has further diversified the market, offering consumers more choices and niche products.

Company Name | Establishment Year | Headquarters |

|---|---|---|

Heineken N.V. | 1864 | Amsterdam, Netherlands |

Carlsberg Group | 1847 | Copenhagen, Denmark |

Diageo Singapore | 1997 | London, United Kingdom |

Pernod Ricard Singapore | 1975 | Paris, France |

AB InBev | 2008 | Leuven, Belgium |

| Asia Pacific Breweries (Tiger Beer) | 1931 | Singapore |

Bacardi Limited | 1862 | Hamilton, Bermuda |

Molson Coors | 1786 | Chicago, Illinois, USA |

Beam Suntory | 1899 | Osaka, Japan |

Moët Hennessy Asia Pacific | 1743 | Paris, France |

Some recent competitor trends and key insights about major players include:

Asia Pacific Breweries: Known for producing Tiger Beer, Asia Pacific Breweries remains a dominant force in Singapore’s beer market. In 2023, the company saw a 10% increase in domestic sales, bolstered by new product launches and marketing campaigns aimed at younger consumers.

Diageo: As a global leader in spirits, Diageo’s premium brands like Johnnie Walker and Tanqueray have maintained strong market positions. In 2023, the company reported a 12% growth in sales in Singapore, driven by increased demand for premium spirits in the hospitality sector.

Pernod Ricard: With a focus on high-end spirits like Chivas Regal and Absolut Vodka, Pernod Ricard saw a 15% increase in sales, particularly in the premium on-trade segment, as luxury venues reopened post-pandemic.

Beam Suntory: Beam Suntory continues to expand its presence in Singapore through its premium whiskey and bourbon offerings. In 2023, the company introduced new craft whiskeys that appeal to Singapore’s affluent and expatriate community, resulting in a 9% increase in sales.

Lion Brewery Co.: A key player in Singapore’s growing craft beer scene, Lion Brewery Co. saw a 20% increase in demand for its locally brewed craft beers in 2023, driven by consumers' preference for unique, artisanal products.

Brass Lion Distillery: Specializing in premium gin, Brass Lion Distillery has captured the attention of Singapore’s cocktail culture. In 2023, the company reported a 30% growth in sales as its products gained traction in high-end bars and restaurants.

What Lies Ahead for Singapore Alcoholic Drinks Market?

The Singapore alcoholic drinks market is expected to see steady growth by 2029, with a respectable CAGR projected during the forecast period. Key drivers include changing consumer preferences, growth in premiumization, and the rise of online alcohol sales.

Increased Demand for Premium Products: As disposable incomes rise and consumers become more discerning, there is a growing preference for premium alcoholic beverages. This shift is expected to be particularly strong in the spirits and wine segments, where consumers seek high-quality products and unique drinking experiences.

Growth in Low-Alcohol and Non-Alcoholic Alternatives: With a rising focus on health and wellness, there is anticipated growth in the demand for low-alcohol and non-alcoholic beverages. Brands are responding by expanding their portfolios to include alcohol-free beers, low-alcohol wines, and other healthier options, meeting the needs of health-conscious consumers.

Technological Integration: The integration of advanced technologies, such as AI-driven recommendation systems and digital marketing, is expected to shape the future of the market. E-commerce platforms, offering a convenient and personalized purchasing experience, are set to increase their market share, making online alcohol sales a key growth driver.

Sustainability Initiatives: Increasing environmental awareness is prompting alcoholic beverage companies to adopt more sustainable practices. This includes using eco-friendly packaging, reducing carbon footprints in production, and supporting responsible drinking campaigns. These practices are expected to appeal to the environmentally conscious consumer base in Singapore, influencing buying decisions.

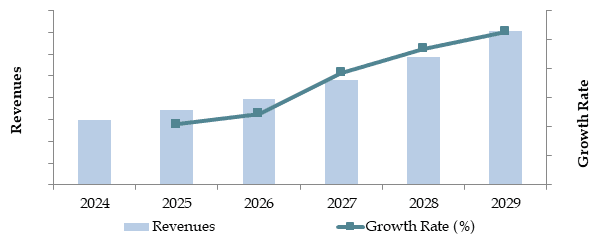

Future Outlook and Projections for Singapore Alcoholic Beverages Market on the Basis of Revenues in USD Billion, 2024-2029

Source: TraceData Research Analysis

Singapore Alcoholic Drinks Market Segmentation

- By Alcohol Type:

- Beer

- Spirits (Whiskey, Vodka, Rum)

- Wine (Red, White, Sparkling)

- Cider

- Ready-to-Drink (RTD) Cocktails

- By Beer

- Lager

- Dark Beer and others

- By Beer

- Craft

- Standard Beer

- By RTDs

- Malt based RTDs

- Spirit Based RTDs

- Wine Based RTDs

- Non-Alcoholic RTDs and others

- By Spirits

- Brandy

- Dark Rum

- White Rum

- Whiskies

- Gin

- Vodka and others

- By Vodka

- Flavoured

- Non-Flavoured Vodka

- By Wine

- Fortified Wine

- Champagne

- Other Sparkling Wine

- Red Wine

- White Wine and others

- By Distribution Channel:

- On-Trade (Bars, Restaurants, Hotels)

- Off-Trade (Supermarkets, Hypermarkets, Convenience Stores)

- By Price Segment:

- Economy

- Mid-Range

- Premium

- Super Premium

- By Consumer Age:

- 18-24

- 25-34

- 35-54

- 55+

- By Region:

o Central Singapore

o Eastern Singapore

o Western Singapore

o Northern Singapore

o Southern Singapore

Players Mentioned in the Report:

Asia Pacific Breweries Ltd

Carlsberg (S) Pte Ltd

Anheuser-Busch InBev NV

Diageo PLC

Pernod Ricard

William Grant & Sons

Brown-Forman Corporation

Heineken N.V.

LVMH Moët Hennessy Louis Vuitton S.E

Key Target Audience:

Alcoholic Beverage Manufacturers

Hospitality and Retail Chains

E-commerce Platforms for Alcohol Sales

Alcoholic Beverage Importers and Distributors

Regulatory Bodies (e.g., Singapore Food Agency)

Research and Development Institutions

Time Period:

Historical Period: 2018-2023

Base Year: 2024

Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, and Challenges they Face

4.2. Business Model Canvas for Singapore Alcoholic Drinks Market

4.3. Consumer Buying Decision Process

5.1. Market Overview and Genesis

5.2. Number of Breweries and Microbreweries, as on Date

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2018-2023

9.1.1. By Beer (Lager, Dark Beer and others), 2018-2023

9.1.1.1. By Lager (Domestic Premium and Imported Premium), 2018-2023

9.1.1.2. By Craft and Standard Beer, 2018-2023

9.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2018-2023

9.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2018-2023

9.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3.2. By Flavoured and Non-Flavoured Vodka, 2018-2023

9.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2018-2023

9.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2023

9.2.1. By Distribution Channel for Off Trade, 2023

9.3. By Region, 2023-2024P

10.1. Customer Landscape and Segment Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Consumer Needs, Preferences, and Pain Points

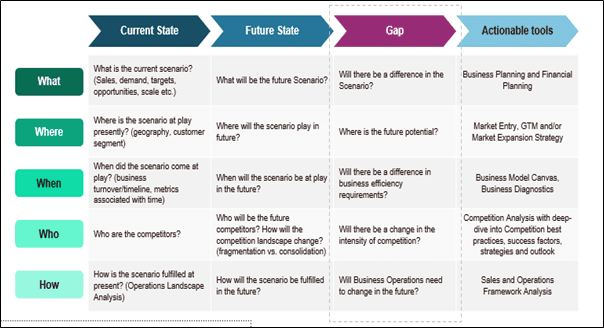

10.4. Gap Analysis Framework

11.1. Trends and Developments in Singapore Alcoholic Drinks Market

11.2. Growth Drivers for Singapore Alcoholic Drinks Market

11.3. SWOT Analysis for Singapore Alcoholic Drinks Market

11.4. Issues and Challenges for Singapore Alcoholic Drinks Market

11.5. Government Regulations for Singapore Alcoholic Drinks Market

13. PEAK Matrix Analysis for Singapore Alcoholic Drinks Market

14.1. Market Share of Key Players in Alcoholic Beverages Market, 2023

14.2. Market Share of Key Players in Beer Market, 2023

14.3. Market Share of Key Players in Wine Market, 2023

14.4. Market Share of Key Players in Spirits Market, 2023

14.5. Market Share of Key Players in RTDs Market, 2023

14.6. Benchmark of Key Competitors in Singapore Alcoholic Drinks Market Basis 15-20 Operational and Financial Parameters

14.7. Strength and Weakness of Key Competitors

14.8. Operating Model Analysis Framework

14.9. Gartner Magic Quadrant for Market Positioning

14.10. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Sales Volume, 2025-2029

16.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2025-2029

16.1.1. By Beer (Lager, Dark Beer and others), 2025-2029

16.1.1.1. By Lager (Domestic Premium and Imported Premium), 2025-2029

16.1.1.2. By Craft and Standard Beer, 2025-2029

16.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2025-2029

16.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2025-2029

16.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3.2. By Flavoured and Non-Flavoured Vodka, 2025-2029

16.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2025-2029

16.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2025-2029

16.2.1. By Distribution Channel for Off Trade, 2025-2029

16.3. By Region, 2025-2029

17.1. Strategic Recommendations

17.2. Opportunity Identification

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all demand and supply side entities for the Singapore Alcoholic Drinks Market. Based on this ecosystem, we will shortlist the leading 5-6 producers in Singapore, considering their financial performance, production capacity, and market share.

Sourcing is conducted through industry reports, articles, and proprietary databases to perform extensive desk research, gathering industry-level insights and relevant data about the market.

Step 2: Desk Research

We conduct exhaustive desk research by referencing various secondary and proprietary databases. This approach enables a comprehensive analysis of the Singapore alcoholic drinks market by aggregating data on sales revenue, market players, product categories, and distribution channels. We also examine company-level data from sources such as annual reports, financial statements, and press releases to build a thorough understanding of the market and its key players.

Step 3: Primary Research

We initiate in-depth interviews with senior executives and other stakeholders from leading Singapore Alcoholic Drinks Market companies, including distributors, retailers, and hospitality sector representatives. These interviews help validate our research hypotheses, authenticate statistical data, and provide valuable operational and financial insights. A bottom-to-top approach is employed to estimate sales volume for each key player, which is then aggregated to project overall market size.

To further validate our findings, we conduct disguised interviews by approaching companies as potential customers, enabling us to cross-check the information shared by company representatives and compare it with secondary sources. This process helps ensure accuracy regarding revenue streams, pricing models, market operations, and value chains.

Step 4: Sanity Check

- We undertake bottom-to-top and top-to-bottom analysis, along with market size modeling exercises, to ensure the consistency and reliability of our findings, ensuring that the market size and forecasts align with industry realities. This sanity check is crucial in verifying the accuracy of our data and projections.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Singapore Alcoholic Drinks Market is expected to grow significantly by 2029, driven by factors such as increasing demand for premium beverages, rising disposable incomes, and the expansion of e-commerce platforms. The market, which reached an estimated value of SGD 1.5 billion in 2023, is poised for steady growth as consumers continue to seek unique and high-quality alcoholic drinks.

Key players in the Singapore Alcoholic Drinks Market include Asia Pacific Breweries, Diageo, Pernod Ricard, Beam Suntory, and Moët Hennessy. These companies dominate the market due to their extensive portfolios, well-established distribution networks, and strong brand recognition. Local craft producers like Lion Brewery Co. and Brass Lion Distillery are also making their mark with innovative products tailored to Singaporean tastes.

The primary growth drivers include the premiumization trend, where consumers are increasingly willing to spend on high-end products, as well as the expansion of digital sales channels that offer convenience and a wider range of product offerings. Tourism also plays a significant role, with Singapore’s status as a global travel hub fueling demand for alcoholic beverages in hotels, bars, and restaurants.

The Singapore Alcoholic Drinks Market faces several challenges, including high excise duties and regulatory restrictions on alcohol sales, such as limited sale hours and restrictions on public consumption. Additionally, increasing health consciousness among consumers is leading to a rise in demand for non-alcoholic alternatives, which may temper the growth of traditional alcoholic beverages.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0