Singapore Autoclaves Market Outlook to 2030

By Autoclave Type, By Technology, By Chamber Volume, By End-User, and By Sales Channel

Report Overview

Report Code

TDR0352

Coverage

Asia

Published

October 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Singapore Autoclaves Market Outlook to 2030 – By Autoclave Type, By Technology, By Chamber Volume, By End-User, and By Sales Channel” provides a comprehensive analysis of the autoclaves market in Singapore. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the autoclaves market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Singapore Autoclaves Market Outlook to 2030 – By Autoclave Type, By Technology, By Chamber Volume, By End-User, and By Sales Channel” provides a comprehensive analysis of the autoclaves market in Singapore. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the autoclaves market. The report concludes with future market projections based on installed base, technology adoption, end-user categories, regions, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

Singapore Autoclaves Market Overview and Size

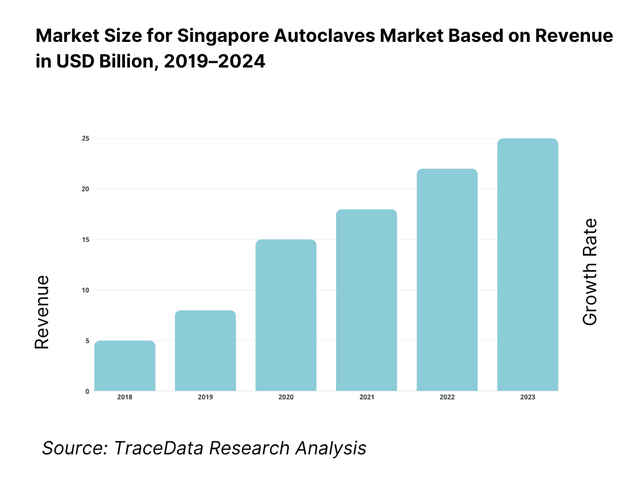

The Singapore autoclave market is valued at USD 0.38 billion in 2023, driven largely by healthcare infrastructure expansion, higher surgical procedure volumes, and increasingly strict regulatory and infection-control standards. Meanwhile, for Singapore specifically, there is a cited figure of approx USD 6.54 million in the steam autoclave segment for 2025 in global reports, with indications that Singapore’s market has been growing steadily as hospitals upgrade CSSDs and biopharma labs invest in clean-steam systems and digital traceability. The global autoclave market as per one source had a CAGR of around 5% from 2019-2023.

Major cities and countries dominating the autoclave and sterilization equipment / services markets include China, India, Japan, South Korea among Asia-Pacific, due to large populations, rapid increases in hospital infrastructure, and strong regulatory push. In Singapore, dominance of the market is driven by the presence of advanced public hospitals, biopharma manufacturing hubs, stringent regulatory oversight by HSA and MOM (for pressure vessels), and high per-capita healthcare investment, resulting in early adoption of higher-grade and feature-rich autoclaves.

What Factors are Leading to the Growth of the Singapore Autoclaves Market:

Hospital throughput and ageing case-mix expanding sterilization demand: Singapore’s acute hospitals operated 11,912 beds, alongside 1,950 psychiatric beds and 2,593 community-hospital beds. Admissions are particularly heavy in older cohorts, with acute hospital admission rates reaching 333.4 per 1,000 residents aged 65+, compared with 84.4 for those aged 15–64. With a resident population of 6,036,900 and 20 acute hospitals, daily surgical and ward instrument reprocessing cycles remain structurally high. This directly lifts autoclave load counts in CSSDs and satellite sterilization rooms across clusters, driving sustained demand for sterilization equipment.

Biomedical manufacturing and investment pipeline supporting GMP autoclaves: Singapore’s manufacturing sector generated S$423.6 billion of total output and S$114.5 billion in value added, with fixed-asset investment commitments of S$13.5 billion expected to create 18,700 jobs. Public-sector R&D expenditure reached S$4,548.3 million, underscoring strong capital and research flows. These flows translate into higher demand for clean-steam, pass-through, and validation-grade autoclaves for biologics, research laboratories, and medical device plants. Such production environments require documented sterilization cycles and batch records under GMP, directly tying market growth to the biomedical investment pipeline.

Clinic and research footprint scaling routine sterilization cycles: Singapore has 1,228 dental clinics and 2,358 general dental practitioners, supported by a resident base of 4,180,900. University and public-sector laboratories drew S$321.9 million in capital expenditure within public R&D, refreshing equipment for biosafety workflows. This high clinic density and active laboratory procurement create steady demand for tabletop Class-B autoclaves and research sterilizers. Frequent cycle turnover for dental instruments, culture media, and waste decontamination ensures continuous utilization, embedding sterilization requirements across both primary care and advanced research ecosystems.

Which Industry Challenges Have Impacted the Growth of the Singapore Autoclaves Market:

Capacity strain requires high uptime and validation cadence: Singapore’s acute inpatient capacity stood at 11,912 beds, with plans to add 13,600 healthcare beds over the medium term. Admission rates among seniors are 333.4 per 1,000 residents, indicating sustained and rising reprocessing loads. In this high-demand environment, autoclave downtime risks procedure delays and operational backlogs. CSSDs must therefore carefully schedule Bowie-Dick tests, leak tests, and calibrations while maintaining availability for theatres and wards across 20 acute hospitals, amplifying the strain on existing sterilization infrastructure.

Infrastructure footprint constraints in dense facilities: Singapore’s population density reached 8,207 persons per sq km, with public providers operating 11 public hospitals in a land-scarce environment. Plant rooms and CSSDs must balance steam supply, condensate routing, and ventilation within limited space allocations. Adding pass-through autoclaves into legacy layouts remains technically challenging, particularly as community hospitals expanded to 2,593 beds and home-hospital programs scaled to 200 MIC@Home beds. These distributed models require sterilization support across multiple nodes, intensifying the pressure on limited healthcare facility footprints.

Service and compliance workload across a broad facility base: Singapore lists 20 acute hospitals and 10 community hospitals, alongside 1,228 dental clinics—each requiring pressure-vessel inspections and sterilization documentation. Authorized Examiner engagement and periodic checks must be coordinated under the pressure-vessel regime, while clinics and labs maintain daily cycle records. With 2,358 general dental practitioners and expanding research facilities supported by S$4,548.3 million in public R&D expenditure, the compliance and servicing workload generated by autoclave fleets is extensive, creating operational bottlenecks for both healthcare providers and distributors.

What are the Regulations and Initiatives which have Governed the Market:

HSA medical-device controls and Essential Principles (sterilization evidence): The Health Sciences Authority requires dealers to maintain records demonstrating conformity, including ISO 13485 quality management compliance and sterilization validation evidence. For sterile Class A devices, documentation must show that autoclaves meet relevant standards. These obligations apply across 20 acute hospitals and 1,228 dental clinics, where demand is shifting toward autoclaves capable of producing auditable cycle records. This strengthens accountability in sterilization and embeds compliance as a driver of procurement decisions.

MOM Pressure Vessel registration and inspection (Authorised Examiner regime): Steam autoclaves are regulated as pressure vessels, requiring registration prior to operation and periodic inspection by an Authorised Examiner. Facilities encompassing 11,912 acute beds and 2,593 community-hospital beds must align equipment commissioning and inspection cycles to avoid disruptions. This framework places an added operational responsibility on hospitals and distributors, ensuring safety and reliability but also increasing administrative and maintenance workloads across Singapore’s healthcare infrastructure.

NEA licensing for biohazardous healthcare waste and TIW collectors: Autoclave-based decontamination for healthcare and research waste falls under the National Environment Agency’s Toxic Industrial Waste framework. Disposal of biohazardous wastes must be managed by licensed collectors under the Environmental Public Health (Toxic Industrial Waste) Regulations. This requirement applies to waste streams emerging from 20 acute hospitals, 10 community hospitals, and 1,228 dental clinics. Licensing rules ensure safe handling and treatment of biomedical waste but also add another compliance dimension to autoclave operations in healthcare and research facilities.

Singapore Autoclaves Market Segmentation

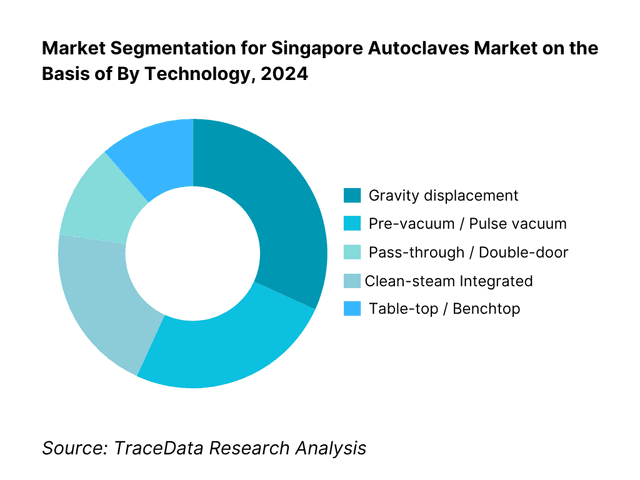

By Technology: Among these, pre-vacuum steam autoclaves tend to dominate in hospitals and high-throughput CSSD environments. This is because they provide better penetration, faster cycle times (especially for porous and wrapped loads), and are more compliant with stringent infection control and regulatory standards. Hospitals that perform large volumes of sterilization load require reliable and quick cycle turnover; pre-vacuum autoclaves also minimize residual moisture and improve safety of sterilization for complex instruments. Table-top benchtop units are more restricted to clinics/dental settings, but their smaller scale means lower revenue contribution compared to hospital-grade pre-vacuum systems in value terms.

By End-User: Public hospitals / CSSDs are the dominant end-user in Singapore’s autoclaves market. They account for the bulk of high-capacity units, rigorous validation and compliance, and tend to invest in full-scale hospital autoclaves (large chamber volume, clean-steam systems, etc.). Private hospitals and day-surgery centres follow, but often with smaller chamber sizes and simpler features. The pharmaceutical and biotech sector is growing, especially in clean room-grade and GMP-compliant autoclaves, but as of now contributes less in volume though higher in price per unit. Dental clinics use mainly tabletop benchtop units. Research labs and universities require versatility and sometimes clean steam, but volumes are lower.

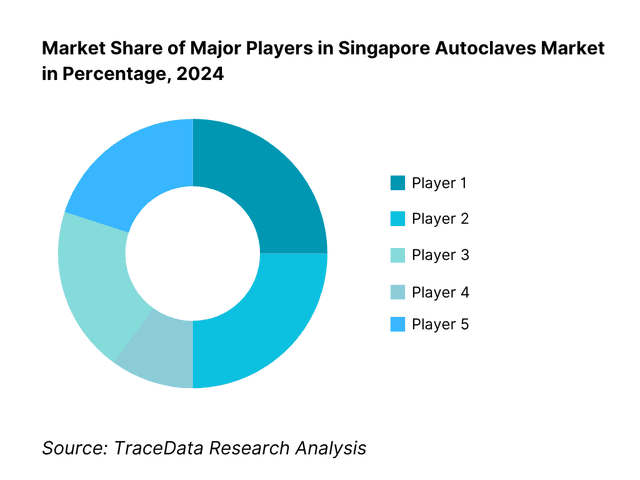

Competitive Landscape in Singapore Autoclaves Market

The autoclaves / steam sterilization / sterilization equipment market is moderately consolidated globally, with a few large OEMs and specialist players dominating hospital and pharma segments. In Singapore, major players are those with strong validation, after-sales service, compliance to international standards (EN, ISO, AAMI), and who partner with public institutions. The high cost of hospital-grade units, regulatory burden, and service & spare parts competency create high barriers to entry.

Name | Founding Year | Original Headquarters |

STERIS | 1985 | Mentor, Ohio, USA |

Getinge AB | 1904 | Getinge, Sweden |

Belimed | 1968 | Zug, Switzerland |

Steelco (Miele Group) | 2001 | Riese Pio X, Italy |

Tuttnauer | 1925 | Breda, Netherlands |

Matachana | 1962 | Barcelona, Spain |

Fedegari | 1953 | Pavia, Italy |

Astell Scientific | 1884 | London, United Kingdom |

Priorclave | 1988 | London, United Kingdom |

MELAG | 1951 | Berlin, Germany |

Midmark / Ritter | 1915 | Versailles, Ohio, USA |

W&H Dentalwerk | 1890 | Berlin, Germany |

Shinva | 1943 | Zibo, Shandong, China |

Consolidated Sterilizer Systems | 1946 | Boston, Massachusetts, USA |

Esco Lifesciences | 1978 | Singapore, Singapore |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

STERIS: A global leader in sterilization solutions, STERIS has recently expanded its portfolio in Singapore by introducing autoclaves integrated with advanced digital monitoring systems, enabling hospitals and biopharma labs to maintain full compliance with CFR audit trails and predictive maintenance.

Getinge AB: Known for its dominance in hospital CSSD solutions, Getinge has reinforced its presence in Singapore by partnering with major public hospitals to deploy large-capacity pass-through autoclaves. The company is also investing in water- and energy-efficient sterilization technologies to align with Singapore’s sustainability mandates.

Belimed: Specializing in hospital and cleanroom sterilization, Belimed has launched a new range of modular autoclaves tailored for compact CSSDs. The brand is gaining traction in Singapore due to its flexible chamber configurations and strong emphasis on validation support for regulatory compliance.

Tuttnauer: A long-standing supplier of tabletop and mid-size autoclaves, Tuttnauer has reported increased adoption in Singapore’s dental and private healthcare sectors. Recent launches include Class-B tabletop autoclaves with automated cycle documentation, targeting clinics looking to upgrade to digital-ready sterilization systems.

Esco Lifesciences: Headquartered in Singapore, Esco has leveraged its local base to strengthen distribution of compact and laboratory autoclaves across universities and research institutes. The company is also focusing on integrating sterilizers into its broader laboratory equipment portfolio, positioning itself as a one-stop provider for life science institutions.

What Lies Ahead for Singapore Autoclaves Market?

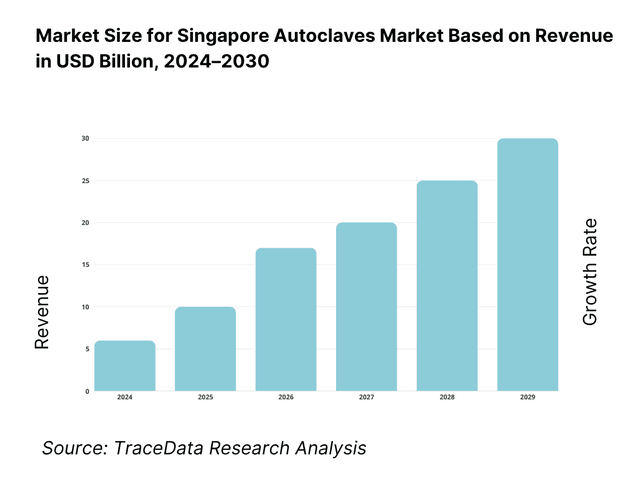

The Singapore autoclaves market is expected to advance steadily by 2030, supported by sustained investment in healthcare infrastructure, the expansion of the biomedical manufacturing sector, and strict regulatory standards governing sterilization and infection control. Growth will be further reinforced by the country’s emphasis on high-quality healthcare delivery, rising surgical workloads, and the continuous push for compliance with global sterilization norms.

Integration of Digital Sterilization Systems: The future of Singapore’s autoclaves market is set to shift toward IoT-enabled sterilizers with remote diagnostics, audit trail capabilities, and predictive maintenance tools. These solutions are driven by hospitals’ and labs’ need for enhanced compliance and reduced downtime.

Adoption of Clean-Steam and Eco-Efficient Models: With Singapore’s healthcare facilities pursuing greener and more sustainable operations, demand for autoclaves equipped with clean-steam generators and water-saving vacuum pumps will grow. Such systems help hospitals meet both infection-control and environmental sustainability targets.

Growth of Biopharma GMP Sterilization Needs: Singapore’s role as a regional biopharmaceutical hub will increase demand for validation-grade autoclaves tailored to cleanroom and GMP production facilities. These units, with specialized cycle configurations, will see higher adoption in Tuas and other biomedical parks.

Emphasis on Customization for Clinics and Research Labs: Smaller healthcare providers, dental clinics, and academic research institutes will increasingly require compact, tabletop autoclaves with cycle flexibility and automated recordkeeping. This demand will drive manufacturers to offer modular solutions tailored to specific end-users.

Singapore Autoclaves Market Segmentation

By Autoclave Type

Tabletop / Class-B (dental & clinics)

Hospital Large Steam Sterilizers (CSSD)

Laboratory/Research Autoclaves

Pharma-GMP / Production Autoclaves

Medical Waste-Treatment Autoclaves

By Technology

Gravity Displacement

Pre-vacuum / Pulse-vacuum

Pass-through / Double-door

Superheated Water (EHW/SHW)

Clean-steam Generator Integrated

By Chamber Volume

≤60 L

60–250 L

250–800 L

≥800 L

By End-User

Public Hospitals / CSSDs

Private Hospitals & Day Surgery Centres

Dental Chains & Clinics

Research Institutes & Universities

Pharmaceutical, Biotech, IVF & Veterinary Labs

By Application / Load Type

Porous & Wrapped Instruments

Hollow/Lumen Devices & MIS Sets

Liquids & Culture Media

Biohazard/Waste Decontamination

Textiles & Rubber/Polymer Goods

By Utility / Steam Source

House Steam Connection

Integrated Clean-steam Generator

Electric Steam Generator (stand-alone)

Hybrid (house + polish/conditioning)

Players Mentioned in the Report:

STERIS

Getinge

Belimed

Steelco (Miele Group)

Tuttnauer

Matachana

Fedegari

Astell Scientific

Priorclave

MELAG

Midmark / Ritter

W&H

Shinva

Consolidated Sterilizer Systems

Esco

Key Target Audience

Procurement Heads of public hospitals in Singapore

Heads of CSSD / Sterilization Units in private hospital groups (e.g. Raffles, Parkway)

Facility / Engineering Managers in pharmaceutical / biotech companies operating in Singapore (e.g. those in Tuas Biomedical Parks)

Heads of Dental Chain networks and dental clinics requiring upgrade to Class-B/Tabletop units

Heads of Research Institutes / University Laboratories requiring clean-steam and validation compliance

Investments & Venture Capitalist Firms interested in medtech / infection control / sterilization equipment markets

Government and Regulatory Bodies

Hospital Group Strategy / Capital Equipment Planning Teams

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Delivery Model Analysis for Autoclaves (direct OEM sales, distributors, MEP contractors, outsourced reprocessing-margins, preferences, strengths, weaknesses)

4.2. Revenue Streams for Autoclaves Market (equipment sales, AMCs, spare parts, validation/calibration, digital monitoring subscriptions)

4.3. Business Model Canvas for Autoclave OEMs & Distributors (partners, activities, value propositions, customer segments, cost structures, revenue streams)

5.1. Freelance Validation Engineers vs Full-Time Service Teams (Authorised Examiners, validation cycles, AMC models)

5.2. Investment Model in Singapore Autoclaves Market (capex purchases, leasing options, bundled AMC/service packages)

5.3. Comparative Analysis of Procurement Funnel (public GeBIZ tendering vs private hospital/direct distributor procurement)

5.4. CSSD Budget Allocation by Facility Size (public hospitals, private groups, day surgery centres, dental clinics)

8.1. Revenues (historical performance, CAGR, public vs private hospitals, dental and lab contributions)

9.1. By Market Structure (in-house CSSD vs outsourced reprocessing)

9.2. By Autoclave Type (tabletop Class-B, large hospital steam, lab/research autoclaves, pharma GMP autoclaves, waste-treatment autoclaves)

9.3. By End-User (public hospitals, private hospitals/day surgery, dental clinics, research institutes/universities, pharma/IVF/veterinary labs)

9.4. By Chamber Volume (≤60 L, 60-250 L, 250-800 L, ≥800 L)

9.5. By Technology (gravity displacement, pre-vacuum, pass-through/double-door, clean steam generators, superheated water systems)

9.6. By Sales Channel (direct OEM, authorised distributors, MEP integrators, public tenders, exports/ASEAN)

9.7. By Region (Central, East, West, North, North-East Singapore)

10.1. Client Landscape and Cohort Analysis (public hospitals, private hospital groups, biopharma hubs, dental clinic chains)

10.2. Procurement Needs and Decision-Making Process (clinical engineering, procurement committees, validation engineers)

10.3. ROI and Effectiveness of Autoclaves (cycle time, utility savings, AMC cost per annum, digital compliance benefits)

10.4. Gap Analysis Framework (CSSD retrofits, day-surgery pipeline, pharma niche requirements, digital audit trail gaps)

11.1. Trends and Developments for Singapore Autoclaves Market (IoT dashboards, RFID integration, water-saving systems, double-door adoption)

11.2. Growth Drivers for Singapore Autoclaves Market (infection control mandates, hospital redevelopment, pharma GMP expansion, lab research growth)

11.3. SWOT Analysis for Singapore Autoclaves Market

11.4. Issues and Challenges for Singapore Autoclaves Market (steam quality, high capex, AE bottlenecks, service downtime, parts lead time)

11.5. Government Regulations for Singapore Autoclaves Market (HSA classification, MOM pressure vessel registration, MOH infection standards, PUB discharge rules, SCDF fire codes)

12.1. Market Size and Future Potential for IoT-Enabled Autoclaves (predictive maintenance, remote monitoring, CFR-compliant records)

12.2. Business Models and Revenue Streams (digital subscriptions, service bundling, validation data storage)

12.3. Delivery Models and Type of Digital Solutions (cloud dashboards, remote QA, digital batch records)

15.1. Market Share of Key Players (basis installed base and revenues)

15.2. Benchmark of Key Competitors (company overview, USP, product portfolio, business model, chamber sizes, AMC terms, pricing, validation compliance, technology features, major clients, marketing strategy, recent developments)

15.3. Operating Model Analysis Framework (direct vs distributor-led, service integration, validation partnerships)

15.4. Gartner Magic Quadrant (execution vs innovation mapping for OEMs and distributors)

15.5. Bowman’s Strategic Clock for Competitive Advantage (pricing vs differentiation positioning)

16.1. Revenues (future projections with CAGR, public/private split)

17.1. By Market Structure (in-house vs outsourced CSSD)

17.2. By Autoclave Type (tabletop, hospital-grade, lab, pharma GMP, waste treatment)

17.3. By End-User (public hospitals, private hospitals, dental clinics, research institutes, pharma/IVF/vet labs)

17.4. By Chamber Volume (≤60 L, 60-250 L, 250-800 L, ≥800 L)

17.5. By Technology (gravity, pre-vacuum, pass-through, clean-steam generator, superheated water)

17.6. By Sales Channel (direct OEM, distributors, MEP integrators, public tenders, ASEAN exports)

17.7. By Region (Central, East, West, North, North-East Singapore)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Singapore Autoclaves Market. Based on this ecosystem, we will shortlist leading 5–6 autoclave suppliers in the country based on their financial information, market reach, and installed base. Sourcing is conducted through ministry portals (MOH/GeBIZ/MOM/HSA), industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the revenues of OEMs and distributors, number of autoclave installations, technology adoption (pre-vacuum, pass-through, clean-steam), service and AMC structures, and demand indicators such as hospital bed capacity, biopharma investments, and laboratory expansions. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and GeBIZ award notices. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Singapore Autoclaves Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate revenue contributions for each player, thereby aggregating to the overall market. As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential clients. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chains, processes, pricing, and other factors.

Step 4: Sanity Check

A bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity of the process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Singapore Autoclaves Market is poised for steady expansion, supported by the country’s advanced healthcare infrastructure, growing biopharmaceutical manufacturing base, and strong regulatory emphasis on infection prevention. With 20 acute hospitals and over 1,200 dental clinics operating nationwide, the demand for sterilization solutions is consistent and growing. The market’s potential is further reinforced by Singapore’s role as a regional biomedical hub, where clean-steam and validation-grade autoclaves are essential for GMP compliance in pharmaceutical and biotech facilities.

The Singapore Autoclaves Market features several global and regional leaders, including STERIS, Getinge, Belimed, Steelco (Miele Group), and Tuttnauer. These companies dominate due to their wide product portfolios, strong presence in hospital CSSDs, and after-sales service networks. Other notable players include Matachana, Fedegari, Astell Scientific, Priorclave, MELAG, Midmark/Ritter, W&H, Shinva, Consolidated Sterilizer Systems, and Esco. Collectively, these players ensure that hospitals, clinics, and laboratories have access to both large-scale sterilization solutions and compact tabletop autoclaves.

Key growth drivers include the rise in hospital admissions—with more than 11,900 acute hospital beds supporting high sterilization throughput—and the expansion of Singapore’s manufacturing output, which reached S$423.6 billion in 2024, driven partly by biopharma investments. Government emphasis on infection-control compliance, through regulatory oversight by the Health Sciences Authority (HSA) and Ministry of Manpower (MOM) for pressure vessels, also accelerates adoption. In addition, Singapore’s 4,500+ million public R&D expenditure supports university and lab procurement of advanced sterilization systems for research and biosafety applications.

The Singapore Autoclaves Market faces several challenges, including high capital intensity, as large hospital autoclaves require significant investment in clean-steam, water, and electrical infrastructure. Compliance with MOM’s pressure vessel inspection regime places administrative and operational burdens on healthcare facilities and distributors. Additionally, land and space constraints—given Singapore’s 8,200 people per sq km density—limit plant room expansions, making retrofits and new installations more complex. Finally, reliance on imported spare parts can extend downtime during critical failures, straining CSSD operations and surgical schedules.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0