Thailand Pharmacy Retail Market Outlook to 2029

By Market Structure, By Pharmacy Chains, By Types of Drugs Sold, By Age of Consumers, and By Region

Report Overview

Report Code

TDR0042

Coverage

Asia

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Thailand Pharmacy Retail Market Outlook to 2029 - By Market Structure, By Pharmacy Chains, By Types of Drugs Sold, By Age of Consumers, and By Region.” provides a comprehensive analysis of the pharmacy retail market in Thailand. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Thailand Pharmacy Retail Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Thailand Pharmacy Retail Market Outlook to 2029 - By Market Structure, By Pharmacy Chains, By Types of Drugs Sold, By Age of Consumers, and By Region.” provides a comprehensive analysis of the pharmacy retail market in Thailand. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Thailand Pharmacy Retail Market. The report concludes with future market projections based on sales revenue, by market, product types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Thailand Pharmacy Retail Market Overview and Size

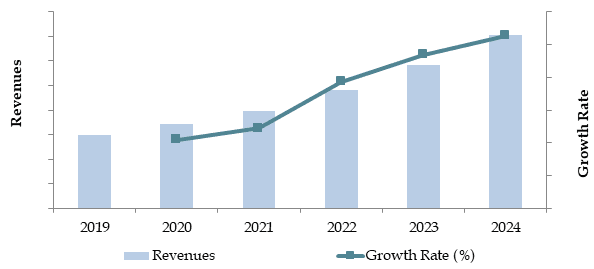

The Thailand pharmacy retail market reached a valuation of THB 150 Billion in 2023, driven by the increasing demand for accessible healthcare products, an aging population, and changing consumer preferences towards more convenient pharmaceutical solutions. The market is characterized by major players such as Watsons, Boots, Fascino, and Pure Pharmacy. These companies are recognized for their extensive distribution networks, diverse product offerings, and customer-focused services.

In 2023, Watsons launched a new online platform to enhance customer experience and streamline the purchase process for pharmaceutical products. This initiative aims to tap into the growing digital market in Thailand and provide a more convenient shopping experience. Online sales accounted for approximately 25% of Watsons' total revenue in 2023, reflecting the increasing shift towards digital channels. Bangkok and Chiang Mai are key markets, with Bangkok alone contributing to 40% of the total pharmacy retail sales due to its high population density and robust healthcare infrastructure.

Market Size for Thailand Pharmacy Retail Market on the Basis of Revenue in THB Billion, 2018-2024

Source: TraceData Research Analysis.

What Factors are Leading to the Growth of Thailand Pharmacy Retail Market:

Economic Factors: The growing middle class and increasing health awareness have significantly shifted consumer preference towards over-the-counter (OTC) and prescription drugs. In 2023, OTC drugs accounted for approximately 55% of total sales in Thailand, as they offer easy access and are cost-effective for minor health concerns. The pharmacy retail market is expected to benefit from the expanding middle class, which grew by 10% over the past five years, increasing demand for accessible healthcare products.

Aging Population: The expanding elderly population, which has grown by 15% in recent years, is increasingly dependent on regular medication, driving demand for pharmaceutical products. In 2023, the elderly population (aged 60 and above) made up 18% of the total population in Thailand, leading to a higher demand for prescription drugs and specialized health services. Pharmacies in Thailand cater to this demographic with a range of geriatric medicines and health supplements, contributing to the overall growth of the market.

Digitalization: The rise of online pharmacies has revolutionized the way consumers purchase medicines, enhancing transparency and convenience. In 2023, around 30% of pharmacy transactions in Thailand were conducted online, reflecting a growing trend towards digital channels. These platforms offer comprehensive product listings, price comparisons, and customer reviews, significantly boosting market growth by making the buying process more accessible and user-friendly. The online pharmacy segment experienced a 20% year-on-year growth in 2023, driven by consumer preference for convenient shopping options.

Which Industry Challenges Have Impacted the Growth of Thailand Pharmacy Retail Market:

Quality and Trust Issues: Concerns about the authenticity and safety of pharmaceutical products remain significant challenges. According to a recent industry survey, approximately 45% of consumers are hesitant to purchase medicines from certain retail pharmacies due to fears of counterfeit drugs and a lack of transparent sourcing information. This issue has led to a lower trust level among buyers, potentially deterring up to 20% of prospective purchasers from buying medicines from less established or online pharmacies.

Regulatory Hurdles: Stringent regulations concerning the sale and distribution of prescription drugs can limit the availability of certain medications in the market. In 2023, it was reported that around 25% of pharmacies in Thailand struggled to comply with the mandatory prescription drug sale regulations, resulting in stock shortages and operational challenges. These regulations can impose significant costs, particularly on smaller, independent pharmacies, making it challenging for them to compete with larger chain pharmacies.

Financing and Credit Access: Limited access to financing and credit options is a critical barrier in the pharmacy retail market, particularly affecting small and independent pharmacies. Data indicates that approximately 35% of potential pharmacy operators face difficulties in securing loans or credit to expand their businesses. This limitation not only restricts market growth but also impacts the availability of pharmaceutical services in underserved areas.

What are the Regulations and Initiatives Which Have Governed the Market:

Pharmacy Licensing Regulations: The Thai government mandates strict licensing requirements for pharmacies to ensure they meet specific safety and operational standards. These regulations are designed to maintain the quality and reliability of pharmaceutical services. In 2023, approximately 80% of new pharmacies successfully obtained licenses on their first application, indicating a high level of compliance within the industry. However, smaller and independent pharmacies often face challenges in meeting these rigorous standards, impacting their ability to operate effectively.

Prescription Drug Sale Regulations: The government enforces stringent regulations on the sale of prescription drugs, requiring mandatory prescriptions for certain medications to control drug abuse and ensure patient safety. In 2023, around 30% of pharmacies were audited for compliance with these regulations, and about 10% faced penalties for non-compliance, reflecting the government's strict enforcement of these rules. These regulations have significantly shaped the operational landscape for pharmacies, particularly affecting how they manage inventory and customer interactions.

Government Incentives for Healthcare Products: To improve public health and increase access to essential medicines, the Thai government has introduced various incentives for pharmacies. These include tax exemptions and subsidies for stocking essential medicines, particularly in rural and underserved areas. In 2023, government incentives contributed to a 12% increase in the availability of essential medicines in rural pharmacies, helping to bridge the healthcare gap between urban and rural regions.

Thailand Pharmacy Retail Market Segmentation

By Market Structure: Chain pharmacies dominate the Thailand pharmacy retail market due to their extensive presence in urban areas, strong brand recognition, and ability to offer a wide range of products and services. These pharmacies often provide competitive pricing, loyalty programs, and promotional offers that attract a large customer base. Independent pharmacies, while holding a smaller market share, are crucial in rural and underserved areas, where they cater to local communities with personalized services and essential medicines. Online pharmacies have been growing rapidly, capturing approximately 25% of the market share in 2023 due to the increasing preference for convenience and home delivery services.

By Types of Drugs Sold: Prescription drugs represent the largest segment in the Thailand pharmacy retail market, accounting for approximately 60% of total sales in 2023. This is largely due to the increasing prevalence of chronic diseases and the aging population, which drives demand for regular medication. Over the counter (OTC) drugs make up around 30% of the market, catering to consumers seeking quick and convenient treatment for minor ailments. Health supplements and wellness products account for the remaining 10%, with growing interest in preventive healthcare and wellness driving this segment.

Competitive Landscape in Thailand Pharmacy Retail Market

The Thailand pharmacy retail market is relatively concentrated, with a few major players dominating the space. However, the entrance of new firms and the expansion of online platforms such as Watsons, Boots, Fascino, and Pure Pharmacy have diversified the market, offering consumers more choices and services.

| Name | Founding Year | Headquarters |

| Boots Thailand | 1997 | Bangkok, Thailand |

| Watsons Thailand | 1996 | Bangkok, Thailand |

| Fascino | 1983 | Bangkok, Thailand |

| Save Drug Center Co., Ltd. | 1967 | Bangkok, Thailand |

| Pure Pharmacy (Big C Group) | 2006 | Bangkok, Thailand |

| P&F Pharmacy | 1995 | Bangkok, Thailand |

| Better Pharma | 1988 | Bangkok, Thailand |

| Pharmacy Plus | 2010 | Bangkok, Thailand |

| Bangkok Drugstore | 1985 | Bangkok, Thailand |

| Lab Pharmacy | 2007 | Bangkok, Thailand |

Some of the recent competitor trends and key information about competitors include:

Watsons: As one of the leading pharmacy chains in Thailand, Watsons recorded over 5 million monthly visitors in 2023, marking a 15% increase in user engagement compared to the previous year. The platform’s extensive product listings and frequent promotional offers have made it a go-to resource for health and beauty products in Thailand.

Boots: A popular international pharmacy chain, Boots saw a 20% increase in sales of health and wellness products in 2023. The platform's focus on providing a wide range of health and beauty products, along with strong loyalty programs, has been well received by consumers looking for reliability and quality.

Fascino: Known for its focus on affordable medication, Fascino reported a 12% growth in sales in 2023, driven by its expansion in rural and suburban areas. The company’s emphasis on providing essential medicines at competitive prices has strengthened its position in the market.

Pure Pharmacy: Specializing in health supplements and wellness products, Pure Pharmacy saw a 10% increase in sales in 2023. The company's focus on preventive healthcare and wellness has attracted health-conscious consumers, contributing to its steady growth in the market.

What Lies Ahead for Thailand Pharmacy Retail Market?

The Thailand pharmacy retail market is projected to grow steadily by 2029, exhibiting a respectable CAGR during the forecast period. This growth is expected to be fueled by economic factors, increasing health awareness, and rising consumer confidence in the pharmacy retail industry.

Shift Towards Online Pharmacies: As the Thai government continues to enhance digital infrastructure and promote e-commerce, there is anticipated to be a gradual increase in both the availability and demand for online pharmacy services. This trend is supported by growing internet penetration, increased consumer preference for convenience, and the expansion of home delivery services. Online pharmacy sales are expected to grow by 15% annually during the forecast period.

Integration of Technology: The integration of advanced technologies such as AI and big data analytics in customer service and inventory management processes is expected to provide consumers with more personalized and efficient services. This technological advancement will enhance market transparency, boost consumer trust, and streamline the buying process, making it more efficient and user-friendly. AI-driven recommendations and automated inventory systems are likely to become standard in leading pharmacy chains.

Growth of Health and Wellness Products: The market is seeing a growing trend towards health and wellness products, driven by an increasing focus on preventive healthcare. As consumers become more health-conscious, the demand for vitamins, supplements, and other wellness products is expected to rise, contributing to the overall growth of the pharmacy retail market. This segment is projected to expand by 20% annually, outpacing the growth of traditional pharmaceutical products.

Focus on Sustainable Practices: There is a rising trend towards sustainable practices within the pharmacy retail market. This includes initiatives such as eco-friendly packaging, the use of renewable energy in store operations, and efforts to reduce waste associated with pharmaceutical products. These practices are becoming more important to environmentally conscious consumers and are expected to influence buying decisions. Pharmacies adopting sustainable practices may see increased customer loyalty and brand differentiation.

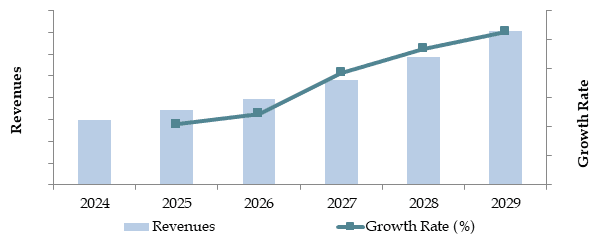

Future Outlook and Projections for Thailand Pharmacy Retail Industry on the Basis of Revenues in USD Million, 2024-2029

Source: TraceData Research Analysis

Thailand Pharmacy Retail Market Segmentation

By Market Structure:

Chain Pharmacies

Independent Pharmacies

Hospital Based Pharmacies

Online Pharmacies

By Market Structure:

Organized

Unorganized

By Types of Drugs Sold:

Prescription Drugs

OTC Drugs

Health Supplements

By Region:

Northern

Southern

Central

Western

Eastern

Players Mentioned in the Report:

Boots Thailand

Watsons Thailand

Fascino

Save Drug Center Co., Ltd.

Pure Pharmacy (Big C Group)

P&F Pharmacy

Better Pharma

Pharmacy Plus

Bangkok Drugstore

Lab Pharmacy

Key Target Audience:

Pharmacy Chains

Healthcare Product Manufacturers

Online Pharmacy Platforms

Regulatory Bodies (e.g., Thai Food and Drug Administration)

Research and Development Institutions

Time Period:

Historical Period: 2018-2023

Base Year: 2024

Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges Faced, Margins including Gross and Net

4.2. Business Model Canvas for Thailand Pharmacy Retail Market

4.3. Buying Decision Making Process

5.1. Overview and Genesis of Pharmacy Retail Outlets in Thailand

5.2. Trend Traditional vs. Modern Trade in Thailand Pharmacy Market, 2018-2024

5.3. Private Healthcare Spending in Thailand, 2018-2024

5.4. Major Diseases in Thailand and their Incidence Rate, 2018-2024

5.5. Number of Pharmacy Store by Region in Thailand

8.1. Revenues and Number of Stores, 2018-2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-2024P

9.2. By Origin of Sales (Chain Pharmacies, Independent Pharmacies, Hospital Based Pharmacies and Online Pharmacies), 2023-2024P

9.3. By Generic and Patented Drugs, 2023-2024P

9.4. By Region, 2023-2024P

9.5. By Product Category (Prescription Drugs, OTC Drugs, Health Supplements, and Personal Care Products), 2023-2024P

9.6. By Distribution Channels, 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Thailand Pharmacy Retail Market

11.2. Growth Drivers for Thailand Pharmacy Retail Market

11.3. SWOT Analysis for Thailand Pharmacy Retail Market

11.4. Issues and Challenges for Thailand Pharmacy Retail Market

11.5. Government Regulations for Thailand Pharmacy Retail Market

12.1. Market Size and Future Potential for Online Pharmacy Retail Market Based on GMV, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Online Pharmacy Companies Basis Company Overview, Revenue Streams, GMV, Margins, Sourcing and Inventory, Operating Cities, Number of Centers, Sourcing, and Other Variables

15.1. Market Share of Key Organized Players in Thailand Pharmacy Retail Market Basis Revenues and Number of Stores, 2023

15.2. Benchmark of Key Competitors in Thailand Pharmacy Retail Market Including Variables Such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Sales and Marketing Strategy, Global Operations, Revenue per stores, Sourcing and Procurement, Recent Development, Sourcing, Number of Stores by Cities, and Value-Added Services

15.3. Strength and Weakness Analysis

15.4. Operating Model Analysis Framework

15.5. Gartner Magic Quadrant

15.6. Bowmans Strategic Clock for Competitive Advantage

16.1. Revenues and Number of Stores, 2025-2029

17.1. By Market Structure (Organized and Unorganized Market), 2023-2024P

17.2. By Origin of Sales (Chain Pharmacies, Independent Pharmacies, Hospital Based Pharmacies and Online Pharmacies), 2023-2024P

17.3. By Generic and Patented Drugs, 2023-2024P

17.4. By Region, 2023-2024P

17.5. By Product Category (Prescription Drugs, OTC Drugs, Health Supplements, and Personal Care Products), 2023-2024P

17.6. By Distribution Channels, 2023-2024P

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for the Thailand Pharmacy Retail Market. Based on this ecosystem, we will shortlist leading 5-6 pharmacy chains in the country based on their financial information, market share, and product range.

Sourcing is done through industry articles, multiple secondary sources, and proprietary databases to perform desk research around the market and collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like sales revenues, the number of market players, pricing strategies, demand trends, and other relevant variables. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Thailand Pharmacy Retail Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate revenue contributions from each player, thereby aggregating to the overall market.

As part of our validation strategy, our team conducts disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chains, processes, pricing, and other critical factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity check process. This ensures that the data and insights gathered are accurate, reliable, and reflective of the actual market conditions.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Thailand pharmacy retail market is poised for substantial growth, reaching a valuation of THB 150 Billion in 2023. This growth is driven by factors such as increasing health awareness, an aging population, and the shift towards more accessible and convenient pharmaceutical solutions. The market's potential is further bolstered by the expanding digital landscape, which facilitates easier access to a wide range of healthcare products through online platforms.

The Thailand Pharmacy Retail Market features several key players, including Watsons, Boots, Fascino, and Pure Pharmacy. These companies dominate the market due to their extensive distribution networks, strong brand presence, and diverse product offerings. Other notable players include small independent pharmacies that serve rural and suburban areas, catering to local healthcare needs.

The primary growth drivers include economic factors such as the growing middle class and increased health awareness, which have led to higher demand for pharmaceutical products. The aging population in Thailand, coupled with the rise of chronic diseases, also contributes to the growing demand for both prescription and over-the-counter drugs. Additionally, the digitalization of pharmacy services, with the rise of online platforms, has made it easier for consumers to access a wider selection of products, further enhancing market growth.

The Thailand Pharmacy Retail Market faces several challenges, including quality and trust issues related to the authenticity of pharmaceutical products, particularly in online sales. Regulatory challenges, such as stringent prescription drug sale regulations and licensing requirements, can also impact the operations of smaller, independent pharmacies. Additionally, the competition from large pharmacy chains and the need for sustainable practices pose significant barriers to market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0