UAE Alcoholic Drinks Market Outlook to 2029

By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region

Report Overview

Report Code

TDR0080

Coverage

Middle East

Published

November 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “UAE Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region.” provides a comprehensive analysis of the alcoholic drinks market in the UAE. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, consumer behavior, challenges, and competitive landscape including key players, market opportunities, and bottlenecks.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “UAE Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region.” provides a comprehensive analysis of the alcoholic drinks market in the UAE. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, consumer behavior, challenges, and competitive landscape including key players, market opportunities, and bottlenecks. The report concludes with future market projections based on sales revenue by market, product types, region, and case studies highlighting key trends and strategies for success.

UAE Alcoholic Drinks Market Overview and Size

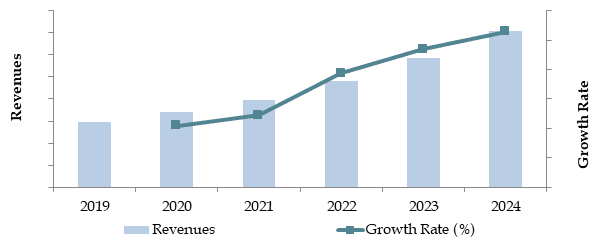

The UAE alcoholic drinks market reached a valuation of AED 12 Billion in 2023, driven by the growing expatriate population, the rise of tourism, and changes in regulatory frameworks that have allowed for more liberalized alcohol consumption laws. Major players include Heineken, Diageo, Anheuser-Busch InBev, and Moët Hennessy. These companies are recognized for their broad product portfolios, innovative marketing strategies, and extensive distribution networks, especially in key urban centers such as Dubai and Abu Dhabi.

In 2023, Anheuser-Busch InBev launched a new premium beer range targeted at the growing middle-class and expat population in the UAE. The product was well-received in both on-trade and off-trade channels, reflecting the evolving consumer preferences towards high-quality, premium alcoholic beverages.

Market Size for UAE Alcoholic Beverage Industry on the Basis of Revenue in USD Billion, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of UAE Alcoholic Drinks Market:

Economic Growth and Expatriate Population: The UAE’s strong economic performance and the significant expatriate population have been key drivers of growth in the alcoholic drinks market. In 2023, expatriates made up over 85% of the population, with many coming from countries where alcohol consumption is a part of their social and cultural lifestyle. This demographic shift has resulted in increased demand for alcoholic beverages across various product categories.

Tourism Boom: The UAE continues to be a global tourism hub, attracting millions of international visitors annually. In 2023, the country recorded over 25 million visitors, many of whom contributed to the robust demand for alcoholic drinks, particularly in the on-trade segment. Luxury hotels, resorts, and bars have been significant beneficiaries of this trend, offering premium alcohol products to meet the demands of high-spending tourists.

Regulatory Liberalization: In recent years, the UAE has seen changes in alcohol-related regulations, such as the removal of alcohol license requirements for residents in some emirates and extended operational hours for alcohol-serving venues. This has made alcohol more accessible to a broader range of consumers, including both residents and tourists. In 2023, sales of alcoholic beverages increased by 12%, reflecting the impact of these regulatory reforms.

Which Industry Challenges Have Impacted the Growth for UAE Alcoholic Drinks Market

Cultural and Religious Sensitivities: The UAE is a predominantly Muslim country, where alcohol consumption is restricted by cultural and religious norms. Although alcohol is available in licensed venues, there are strict regulations governing its sale and consumption, particularly during religious holidays and in certain emirates. These limitations can affect the overall market size, with certain segments of the population abstaining from alcohol altogether. In 2023, cultural sensitivities were noted as a significant barrier, especially for off-trade sales.

Regulatory Restrictions: The UAE imposes stringent regulations on the sale and distribution of alcoholic drinks, including high taxes and licensing fees. In 2023, excise taxes on alcohol were as high as 50%, significantly increasing the cost for consumers. These taxes, along with strict advertising and promotional regulations, limit market growth, particularly for smaller players who face challenges competing with established brands that can absorb higher operational costs.

Health and Wellness Trends: Globally, there is a growing shift towards healthier lifestyles, with consumers increasingly mindful of their alcohol consumption. In the UAE, this trend has led to a rise in demand for low-alcohol and alcohol-free beverages. While this presents an opportunity for market diversification, it also poses a challenge for traditional alcoholic drink categories, as consumers reduce their overall alcohol intake. In 2023, the demand for alcohol-free alternatives grew by 15%, impacting sales of regular alcoholic beverages.

What are the Regulations and Initiatives which have Governed the Market:

Alcohol Licensing Laws: The UAE government strictly regulates the sale and distribution of alcohol through a licensing system. Only licensed hotels, restaurants, and bars are allowed to serve alcohol, and residents must obtain personal alcohol licenses to purchase alcoholic drinks for home consumption. In 2023, regulatory changes made alcohol licenses easier to obtain for residents, which contributed to a 10% increase in off-trade sales.

Excise Tax on Alcohol: The UAE imposes a high excise tax on alcoholic beverages, currently set at 50%. This tax was introduced as part of the government’s efforts to reduce harmful consumption behaviors and generate additional public revenue. The excise tax has driven up the retail prices of alcoholic drinks, impacting overall consumption levels, especially in the mid- to lower-income segments.

Tourism and Hospitality Regulations: Alcohol is a key component of the UAE's tourism and hospitality industry, and regulations are in place to govern the serving of alcohol in hotels, resorts, and designated tourist areas. These regulations require alcohol-serving venues to comply with strict licensing conditions, including ensuring alcohol is not served to minors or visibly intoxicated individuals. In 2023, the government introduced new measures to streamline the approval process for alcohol licenses in tourist hubs like Dubai and Abu Dhabi.

UAE Alcoholic Drinks Market Segmentation

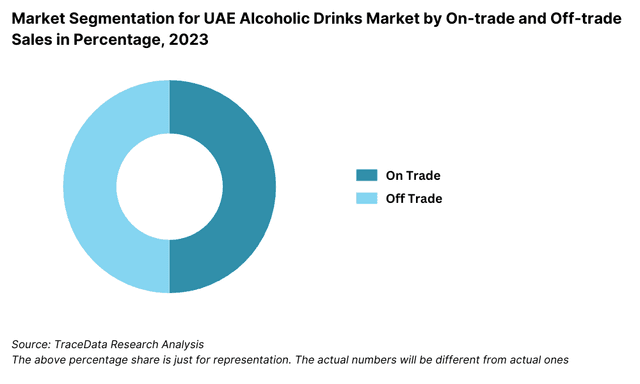

By Distribution Channel: The on-trade segment dominates the UAE alcoholic drinks market, driven by the country's vibrant hospitality industry, including hotels, bars, and restaurants. These venues cater to both the expatriate population and tourists, offering a wide range of premium alcoholic beverages. The off-trade segment, which includes supermarkets and specialized liquor stores, is also significant but remains more restricted due to licensing requirements and cultural factors. In 2023, the on-trade market accounted for approximately 60% of total sales, reflecting the strong influence of tourism and high-end hospitality services.

By Product Type: Beer is the most consumed alcoholic drink in the UAE, favored for its lower alcohol content and wide availability. Spirits follow closely, especially in premium venues where expatriates and tourists prefer high-end brands like whiskey, vodka, and rum. Wine, particularly in the luxury segment, is also popular, with increasing demand for premium and sparkling wines among affluent consumers. In 2023, beer accounted for about 45% of total alcoholic beverage sales, with spirits at 35% and wine at 20%.

%2520in%2520Percentage%252C%25202023.png&w=640&q=75)

By Consumer Demographics: Expatriates form the largest consumer group in the UAE's alcoholic drinks market due to their more liberal consumption habits. Tourists, especially those from Europe and North America, also significantly contribute to sales, particularly in on-trade venues. Local Emiratis, while restricted by religious practices, represent a small but growing segment as the market introduces alcohol-free and low-alcohol options. In 2023, expatriates and tourists combined accounted for approximately 85% of total alcoholic drinks consumption.

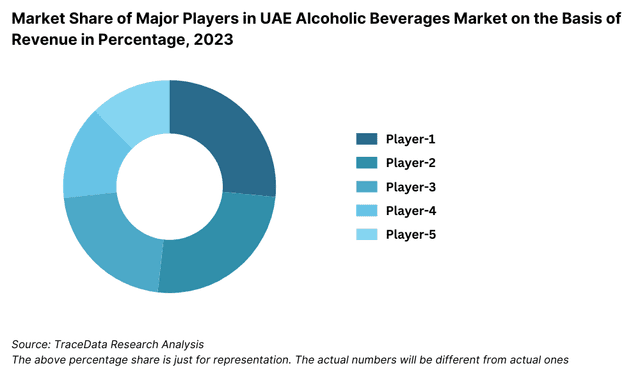

Competitive Landscape in UAE Alcoholic Drinks Market

The UAE alcoholic drinks market is highly competitive, with major international players dominating the space. However, the market has seen the entry of new brands and the growth of local distributors, particularly in the premium and non-alcoholic beverage segments. Key players include multinational beverage giants such as Heineken, Diageo, Anheuser-Busch InBev, and Moët Hennessy. These companies maintain a strong presence through wide product offerings and strategic partnerships with hotels, restaurants, and retailers.

Company Name | Establishment Year | Headquarters |

|---|---|---|

Heineken N.V. | 1864 | Amsterdam, Netherlands |

Carlsberg Group | 1847 | Copenhagen, Denmark |

Diageo Middle East | 1997 | London, United Kingdom |

Pernod Ricard Gulf | 1975 | Paris, France |

AB InBev | 2008 | Leuven, Belgium |

Molson Coors | 1786 | Chicago, Illinois, USA |

Bacardi Limited | 1862 | Hamilton, Bermuda |

Brown-Forman | 1870 | Louisville, Kentucky, USA |

Suntory Beverage & Food | 1899 | Tokyo, Japan |

Constellation Brands | 1945 | Victor, New York, USA |

Recent Competitor Trends and Key Information:

Heineken: Heineken has maintained a strong position in the UAE market by leveraging its well-known brand and wide distribution network. In 2023, the company launched a new premium beer range, which was particularly well-received in Dubai and Abu Dhabi. Heineken has also invested in alcohol-free alternatives, catering to the growing demand for healthier drink options.

Diageo: As a leading global producer of spirits, Diageo continues to dominate the premium alcohol segment in the UAE, with brands such as Johnnie Walker, Tanqueray, and Baileys being particularly popular in high-end hotels and resorts. In 2023, Diageo saw a 15% increase in sales, driven by the growing tourist population and rising demand for premium spirits.

Anheuser-Busch InBev: Known for its flagship brand Budweiser, Anheuser-Busch InBev has been expanding its footprint in the UAE through a focus on both alcoholic and alcohol-free beverages. In 2023, the company reported a 10% growth in sales, fueled by increased distribution in the off-trade sector and partnerships with local retail chains.

Moët Hennessy: The luxury arm of LVMH, Moët Hennessy, continues to dominate the premium wine and champagne segment in the UAE. In 2023, the company introduced limited-edition products targeted at the ultra-luxury market, particularly in Dubai's luxury hotels and events. This strategy has bolstered its image as the leading player in the high-end alcohol market.

MMI (Maritime & Mercantile International): MMI, a UAE-based distributor, remains a key player in the local market. In 2023, MMI expanded its operations by opening new retail outlets in major urban centers, including Dubai and Abu Dhabi. The company focuses on offering a wide range of international and local alcohol brands, catering to both expatriates and tourists.

What Lies Ahead for UAE Alcoholic Drinks Market?

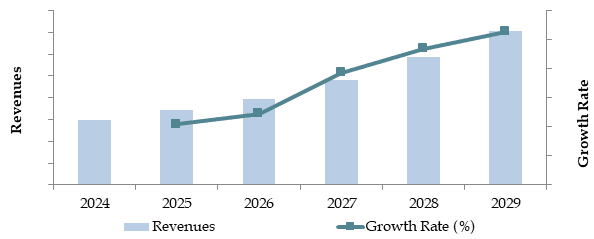

The UAE alcoholic drinks market is projected to experience steady growth by 2029, driven by the expansion of tourism, regulatory reforms, and evolving consumer preferences. The market is expected to achieve a respectable CAGR during the forecast period, supported by economic growth and increasing demand for premium alcoholic beverages.

Shift Towards Low-Alcohol and Alcohol-Free Beverages: As health-consciousness rises among UAE consumers, there is expected to be a gradual shift towards low-alcohol and alcohol-free beverages. This trend aligns with global health and wellness movements, and major alcohol brands have already started to expand their portfolios to include such products. By 2029, this segment is anticipated to account for a larger share of the overall market.

Technological Integration in Retail and Hospitality: The use of AI and digital platforms in retail and hospitality venues will enhance the customer experience and improve operational efficiency. From personalized drink recommendations to automated inventory management, technology is set to streamline the sales process, increase customer engagement, and boost market growth.

Growth in Premiumization: The demand for premium and luxury alcoholic beverages is expected to rise, particularly in high-end hotels, resorts, and restaurants. Affluent tourists and expatriates will continue to drive demand for exclusive spirits, wines, and champagnes. By 2029, premium alcoholic drinks are likely to command a greater share of market revenues.

Sustainability and Environmental Practices: Sustainability initiatives are gaining importance within the UAE alcoholic drinks market. Companies are expected to adopt eco-friendly practices, including reducing packaging waste, improving energy efficiency in production, and offering organic or ethically sourced alcohol products. These efforts will cater to the growing number of environmentally conscious consumers.

Future Outlook and Projections for UAE Alcoholic Beverages Market on the Basis of Revenues in USD Billion, 2024-2029

UAE Alcoholic Drinks Market Segmentation

- By Alcohol Type:

- Beer

- Spirits (Whiskey, Vodka, Rum)

- Wine (Red, White, Sparkling)

- Cider

- Ready-to-Drink (RTD) Cocktails

- By Beer

- Lager

- Dark Beer and others

- By Beer

- Craft

- Standard Beer

- By RTDs

- Malt based RTDs

- Spirit Based RTDs

- Wine Based RTDs

- Non-Alcoholic RTDs and others

- By Spirits

- Brandy

- Dark Rum

- White Rum

- Whiskies

- Gin

- Vodka and others

- By Vodka

- Flavoured

- Non-Flavoured Vodka

- By Wine

- Fortified Wine

- Champagne

- Other Sparkling Wine

- Red Wine

- White Wine and others

- By Distribution Channel:

- On-Trade (Bars, Restaurants, Hotels)

- Off-Trade (Supermarkets, Hypermarkets, Convenience Stores)

- By Price Segment:

- Economy

- Mid-Range

- Premium

- Super Premium

- By Consumer Age:

- 18-24

- 25-34

- 35-54

- 55+

- By Region:

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates (Ras Al Khaimah, Fujairah, Umm Al Quwain, Ajman)

- Western Region

Players Mentioned in the Report:

- Anheuser-Busch InBev

- Heineken N.V.

- Diageo PLC

- Pernod Ricard SA

- Bacardi Limited

- William Grant & Sons Group

- Brown-Forman Corporation

- LVMH Moët Hennessy Louis Vuitton S.E

Key Target Audience:

- Alcoholic Beverage Manufacturers

- Retailers (Supermarkets, Liquor Stores)

- Hotels, Bars, and Restaurants

- Regulatory Bodies (e.g., Dubai Municipality)

- Hospitality and Tourism Operators

- E-Commerce Platforms

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, and Challenges they Face

4.2. Business Model Canvas for UAE Alcoholic Drinks Market

4.3. Consumer Buying Decision Process

5.1. Market Overview and Genesis

5.2. Number of Breweries and Microbreweries, as on Date

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2018-2023

9.1.1. By Beer (Lager, Dark Beer and others), 2018-2023

9.1.1.1. By Lager (Domestic Premium and Imported Premium), 2018-2023

9.1.1.2. By Craft and Standard Beer, 2018-2023

9.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2018-2023

9.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2018-2023

9.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3.2. By Flavoured and Non-Flavoured Vodka, 2018-2023

9.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2018-2023

9.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2023

9.2.1. By Distribution Channel for Off Trade, 2023

9.3. By Emirates, 2023-2024P

10.1. Customer Landscape and Segment Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Consumer Needs, Preferences, and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments in UAE Alcoholic Drinks Market

11.2. Growth Drivers for UAE Alcoholic Drinks Market

11.3. SWOT Analysis for UAE Alcoholic Drinks Market

11.4. Issues and Challenges for UAE Alcoholic Drinks Market

11.5. Government Regulations for UAE Alcoholic Drinks Market

14.1. Market Share of Key Players in Alcoholic Beverages Market, 2023

14.2. Market Share of Key Players in Beer Market, 2023

14.3. Market Share of Key Players in Wine Market, 2023

14.4. Market Share of Key Players in Spirits Market, 2023

14.5. Market Share of Key Players in RTDs Market, 2023

14.6. Benchmark of Key Competitors in UAE Alcoholic Drinks Market Basis 15-20 Operational and Financial Parameters

14.7. Strength and Weakness of Key Competitors

14.8. Operating Model Analysis Framework

14.9. Gartner Magic Quadrant for Market Positioning

14.10. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Sales Volume, 2025-2029

16.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2025-2029

16.1.1. By Beer (Lager, Dark Beer and others), 2025-2029

16.1.1.1. By Lager (Domestic Premium and Imported Premium), 2025-2029

16.1.1.2. By Craft and Standard Beer, 2025-2029

16.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2025-2029

16.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2025-2029

16.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3.2. By Flavoured and Non-Flavoured Vodka, 2025-2029

16.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2025-2029

16.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2025-2029

16.2.1. By Distribution Channel for Off Trade, 2025-2029

16.3. By Emirates, 2025-2029

17.1. Strategic Recommendations

17.2. Opportunity Identification

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the UAE Alcoholic Drinks Market. Based on this ecosystem, we will shortlist leading 5-6 producers in the country, focusing on their financial performance, production capacity/volume, and market influence.

Data sourcing is done through industry articles, government reports, multiple secondary, and proprietary databases to perform extensive desk research around the market and collate industry-level information.

Step 2: Desk Research

We engage in an exhaustive desk research process by referencing a wide range of secondary and proprietary databases. This approach allows us to conduct a detailed analysis of the market, gathering industry-level insights. We delve into key aspects such as sales revenues, market players, pricing trends, demand, and consumer preferences. This analysis is supplemented by company-level research, relying on sources such as press releases, annual reports, and financial statements. This step builds a strong understanding of both the market dynamics and the individual companies within it.

Step 3: Primary Research

In this phase, we conduct in-depth interviews with C-level executives and other stakeholders from key players in the UAE Alcoholic Drinks Market, including producers, distributors, retailers, and industry experts. These interviews serve to validate market assumptions, confirm statistical data, and extract valuable insights on operational and financial aspects of the market. A bottom-to-top approach is used to estimate volume sales for each major player, which is then aggregated to provide an overall market estimate.

To further strengthen the validation process, our team undertakes disguised interviews by contacting industry representatives as potential customers. This approach helps validate operational and financial data shared by company representatives and corroborate it against secondary research sources.

Step 4: Sanity Check

- Finally, we conduct a sanity check through both bottom-to-top and top-to-bottom analysis, along with market size modeling exercises. This ensures the accuracy of our findings and provides a reliable market estimate. The results are cross-checked with industry benchmarks and comparable markets to confirm the validity of the data and projections.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The UAE alcoholic drinks market is expected to see steady growth through 2029, driven by an expanding tourism industry, rising expatriate population, and regulatory reforms that have increased the accessibility of alcohol. The market’s potential is further enhanced by a growing demand for premium and alcohol-free alternatives, aligning with global health and wellness trends. In 2023, the market was valued at AED 12 billion and is projected to grow at a healthy CAGR during the forecast period.

The UAE alcoholic drinks market is dominated by key players such as Heineken, Diageo, Anheuser-Busch InBev, and Moët Hennessy. Local distributors like MMI (Maritime & Mercantile International) and African + Eastern also play significant roles in distributing a wide range of international brands. These companies hold a strong market presence due to their extensive distribution networks, established partnerships with hotels and restaurants, and diverse product offerings.

Key growth drivers include the flourishing tourism sector, particularly in Dubai and Abu Dhabi, where alcohol sales in luxury hotels and restaurants have increased. Changes in alcohol licensing laws have also made alcoholic drinks more accessible to both expatriates and tourists. Additionally, there is rising demand for premium and luxury alcoholic beverages, alongside a growing trend toward low-alcohol and alcohol-free options.

Challenges in the UAE alcoholic drinks market include stringent regulatory restrictions, high excise taxes on alcoholic beverages, and cultural sensitivities surrounding alcohol consumption. These factors limit the market's size and accessibility in certain emirates. Furthermore, the growing health-consciousness among consumers and the rising demand for alcohol-free alternatives could negatively impact sales in traditional alcohol segments.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0